If you’re in need of cash, you might think about obtaining a personal loan, which offers a one-time payment. However, you might want to think about a line of credit if you’re unsure about how much money you might need.

A line of credit is a type of revolving credit that gives you access to funds whenever you need them, up to a predetermined amount. Once the money is returned, you can borrow up to that amount once more. Find out more about lines of credit, their various varieties, when to avoid them, and how to take advantage of them.

How we make money

You have money questions. Bankrate has answers. For more than 40 years, our professionals have assisted you in managing your finances. We always work to give customers the professional guidance and resources they need to be successful on their financial journey.

Because Bankrate adheres to strict editorial standards, you can rely on our content to be truthful and accurate. Our team of distinguished editors and reporters produces truthful and precise content to assist you in making wise financial decisions. Our editorial team produces factual, unbiased content that is unaffected by our sponsors.

By outlining our revenue streams, we are open and honest about how we are able to provide you with high-quality material, affordable prices, and practical tools.

Bankrate. com is an independent, advertising-supported publisher and comparison service. We receive payment when you click on specific links that we post on our website or when sponsored goods and services are displayed on it. Therefore, this compensation may affect the placement, order, and style of products within listing categories, with the exception of our mortgage, home equity, and other home lending products, where legal prohibitions apply. The way and location of products on this website can also be affected by other variables, like our own unique website policies and whether or not they are available in your area or within your own credit score range. Although we make an effort to present a variety of offers, Bankrate does not contain details about all financial or credit products or services.

Two comparable forms of revolving credit are credit cards and lines of credit. With both, you are authorized to borrow up to a predetermined amount, but you are not required to start borrowing right away. You are free to decide how much and when to borrow money, up to the account limit. As long as you don’t owe more than the maximum, you can borrow money again and again; interest will only be charged on the amount you borrow.

But there are some significant distinctions between a credit card and a line of credit. Here’s what you need to know.

Line of credit vs. credit card

One of the most obvious distinctions between the two is that, although a credit card is linked to a line of credit and gives you access to it, you can open a line of credit without a credit card. In general, credit cards are lines of credit, but not all credit cards are lines of credit.

Credit terms and limits

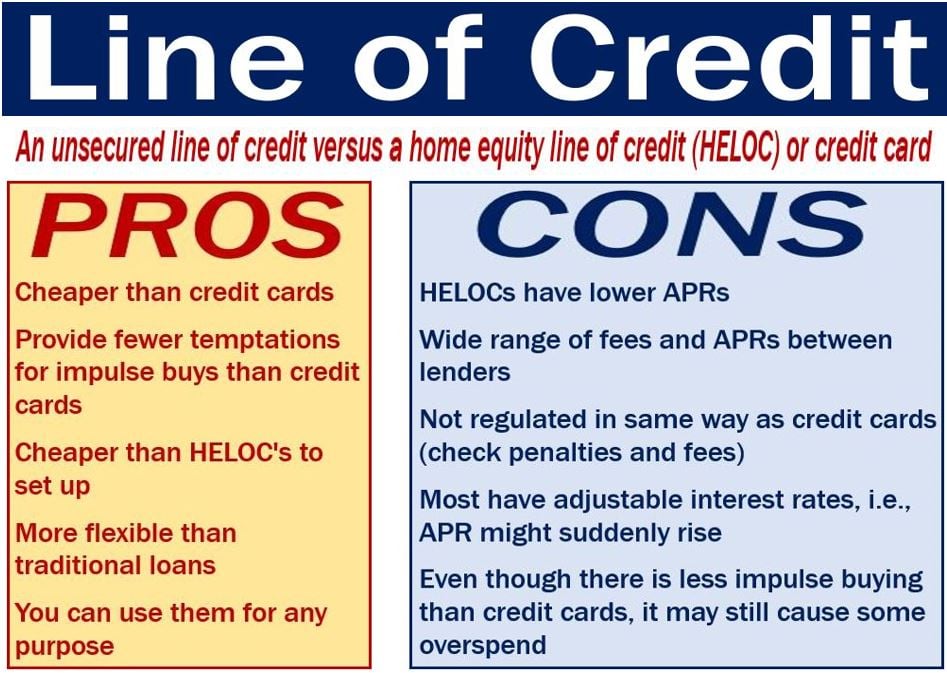

The APR on a line of credit is frequently lower than the APR on credit cards, though terms can vary by lender. Additionally, a line of credit may have a higher credit limit than a credit card. Credit lines might be a better option for large purchases that you plan to pay off over time because of these benefits.

Credit cards offer a practical means of making regular purchases. They frequently offer you a grace period, which isn’t available for credit lines, during which you can avoid paying interest. Additionally, a lot of credit cards provide rewards for spending, such as cash back, that credit lines do not.

When you apply for a credit card, you have to give accurate financial information, but when you apply for a line of credit without a credit card, you usually have to provide proof of income. This implies that applying for a credit line may be a little more difficult and time-consuming.

What is a line of credit?

One type of financial product that lets you borrow money repeatedly is a line of credit. After borrowing up to a predetermined amount, you must pay back what you borrowed. As long as the amount you owe stays below your limit, you can keep using the line of credit. You might be assessed a fee for using a credit line, and interest will be charged on any money you borrow.

How does a line of credit work?

You will receive checks from your issuer that you can write to access your credit line. You can also request a transfer in person, over the phone, or online through your bank to have money deposited into your account. Additionally, you might be able to set up an automatic credit line draw from your bank or credit union to pay for overdrafts on your checking account.

Lines of credit can be secured or unsecured. For instance, your house serves as collateral for home equity lines of credit (HELOC). Typically, HELOCs have variable interest rates; however, banks occasionally provide a fixed-rate option for all or a portion of your balance.

There’s usually a draw period associated with HELOCs, which is the amount of time you can borrow money. You might be given a window of time during which to make payments after the draw period, or you might be forced to pay the whole amount you owe immediately away.

A personal line of credit (PLOC) is typically not secured. You might need to have an active checking account with the bank or credit union issuing the credit line in order to be approved. Following your loan, you will receive a bill every month, and you will have to pay the minimum amount due each month. Generally speaking, the interest rate can change based on the state of the market.

Does a line of credit affect your credit score?

Your credit score may be impacted by opening a new credit line in both positive and negative ways, which may have an impact on how you handle that credit going forward. Here’s how a line of credit affects your credit score:

- New inquiry. A hard inquiry is made by the lender on your credit history when you apply for a line of credit. This inquiry can stay on your credit report for up to two years and have an effect on your FICO score for up to a year.

- Length of credit history. The average age of your accounts decreases when you open a new line of credit. This can have a negative impact on your credit score, especially if you don’t have a long credit history.

- Credit mix. Opening a credit line adds a revolving credit account to your credit history. If you had no prior revolving accounts, this can help your credit mix. Possessing a diverse range of accounts could potentially improve your credit score.

- Amounts owed. Using a personal line of credit has an impact on your credit utilization ratio, which measures how much of your available credit is revolving. Your credit score may be impacted by having a lot of debt from other accounts or a home equity loan.

- Payment history. While late or missed payments will probably result in a decline in your credit score, making on-time monthly payments on your line of credit builds your payment history and can raise your score.

When should you use a personal line of credit?

When you need to pay for an emergency, make a big purchase, or are unsure of how much money you will need to borrow up front, a personal line of credit can be helpful. For example, you might have to pay for unanticipated medical expenses or home repairs, but you’re not sure how much it will all end up costing.

When it comes to carrying a sizable balance that you must pay off over time, a personal line of credit may offer better terms than a credit card and offer you greater flexibility than an installment loan.

What is a credit card?

Using a credit card, you can make regular purchases in-person, over the phone, and online by drawing from a line of credit. Payments can be made with a card by physically inserting, tapping, or swiping it at a terminal, or by using an online payment form and entering the card number, security code, and expiration date. These payments increase the account balance and deduct the purchase amount from the available credit.

How does a credit card work?

Each billing cycle, cardholders will receive an account statement. Many credit cards have a grace period during which interest is not assessed if the full amount is paid by the due date. The cardholder will forfeit the grace period and interest will start to accrue if they don’t pay the entire balance. Every billing cycle, cardholders are required to make at least a minimum payment by the due date; otherwise, they risk late fees and possibly even a penalty annual percentage rate.

When you charge purchases to certain credit cards, you can accrue rewards. Depending on the card, you could be able to use the cash back, points, or miles you accrue on purchases to get gift cards, merchandise, travel, and other things.

How does a credit card affect your credit score?

Similar to a line of credit, a credit card account can have an impact on your credit score. Your credit score can be impacted by a credit card in the following ways:

- New inquiry. A hard inquiry is made when you apply for a new credit card, and this can temporarily lower your credit score.

- Length of credit history. Creating a new account lowers the average age of your existing accounts, which may also slightly reduce your score.

- Credit mix. Getting a new credit card grants you a revolving account, just like a line of credit does. This enhances your credit mix and could improve your score if you have never had any revolving credit on your record.

- Amounts owed. Using credit cards for purchases raises your credit utilization ratio. Your credit score may suffer if it appears that you could exhaust all of your available credit due to a high credit utilization ratio. Generally speaking, if you want to keep your credit score high, you should keep your credit utilization ratio below 30%.

- Payment history. Making on-time credit card payments every billing cycle has a positive impact on your payment history and can raise your credit score. Your score won’t suffer if you pay off the remaining amount in full.

When should you use a credit card?

When you want to have a way to make payments without carrying cash on you, credit cards come in handy. If you can pay off your credit card debt in full each month, using a credit card for regular purchases is a wise decision. In this manner, interest payments are avoided, and credit card debt that is unaffordable to settle is prevented.

Getting paid for your purchases with a top rewards credit card is a terrific idea, especially if you can earn a lot of points in areas where you usually spend money, like dining out, groceries, or gas. Alternatively, if you plan to make a big purchase, it may be worthwhile to look for a credit card that allows you to pay off the balance over time without incurring interest and offers a 0 percent intro APR on purchases for a restricted period of time.

Debit cards and other payment methods may not offer the same level of protection against fraud as credit cards. Most credit card issuers offer cardholders $0 fraud liability. Thus, when traveling or making purchases online, a credit card is frequently a wise option if security is a concern.

Should you consider alternatives to credit?

It could be time to look into alternatives to borrowing if you’ve thought about getting a credit card or a personal line of credit but neither seems like a great option.

- Work on saving. One strategy is to avoid financing a large purchase by building up savings for it. The disadvantage is that you won’t be able to purchase the item until you have enough money. On the plus side, you won’t pay interest.

- Find community resources. Check to see if there are any mutual aid or freecycle groups in your area. These groups occasionally sell used appliances or furniture that other members of the group no longer need.

- Rent what you need. Consider renting a product if you can’t afford to buy something you’ll need for a short while. You can rent a broad range of items, including wedding gowns, textbooks, home improvement tools, and sports equipment.

- Ask for a direct payment plan. You could ask for assistance if you require money for essentials like utility bills or medical expenses. People who are unable to pay the full price are frequently given financial assistance by hospitals and utility companies. They might provide you with a payment plan with better terms than a bank or credit card issuer if you aren’t eligible for a discount.

FAQ

What is credit line in credit card?

The maximum amount that a credit card user may charge to their account, including purchases, balance transfers, cash advances, fees, and interest, is known as their credit line.

What is a $200 credit line?

The maximum amount you can charge to your credit card account, including purchases, balance transfers, cash advances, fees, and interest, is $200. When referring to a credit card, “credit limit” is synonymous with “credit line.”

What does it mean when your credit line is $500?

First and foremost, it’s critical to realize that your credit limit represents the highest amount of money a lender will allow you to borrow. Therefore, if your credit limit is $500, you have up to $500 in available credit before you hit your limit.

How does a line of credit work?

You can get money “on demand” with a line of credit, which can help with unforeseen auto repairs or home projects. Lenders like banks and credit unions usually offer lines of credit, which allow you to access funds for a predetermined amount of time, provided you meet the eligibility requirements.

Read More :

https://www.bankrate.com/finance/credit-cards/line-of-credit-vs-credit-card/

https://wallethub.com/answers/cc/what-is-a-credit-line-on-a-credit-card-2140703642/