One of the most common inquiries regarding credit reports is: How long does information remain on my Equifax credit report? The response varies based on the kind of information and whether it’s regarded as “positive” or “negative.” ”.

Negative information generally remains on credit reports for about seven years, including late or missed payments, accounts that have been reported to collection agencies, accounts that are not paid as agreed upon, and bankruptcies. The various categories of “negative” information and the duration for which they should remain on your Equifax credit report are broken down here:

The following are some instances of “positive” data and the duration for which it remains on your Equifax credit report:

Lastly, when a prospective lender, creditor, or service provider asks for a copy of your Equifax credit report in response to a request for credit or specific services, that request is known as a hard inquiry. These might stay on your credit report from Equifax for a maximum of two years.

It’s crucial to regularly check your Equifax credit report to make sure all of the information is correct and up to date and to make sure that any negative information has been removed from it after the relevant amount of time. Every 12 months, you can get a free copy of your credit report from each of the three national credit bureaus by going to www. annualcreditreport. com. Additionally, you can open a myEquifax account to receive six complimentary Equifax credit reports annually. Additionally, you can sign up for Equifax Core CreditTM to receive a free monthly Equifax credit report and a free monthly VantageScore® 3 by clicking “Get my free credit score” on your myEquifax dashboard. 0 credit score, based on Equifax data. A VantageScore is one of many types of credit scores.

Hard Inquiry: Two Years

A hard inquiry occurs when you apply for credit and the lender requests your complete credit report from a credit bureau. It is also referred to as a hard credit check or hard pull. Although that information isn’t always bad, it can lower your credit score by a few points, and making too many hard inquiries will accumulate. Thankfully, they are only visible on your credit report for two years after the date of the inquiry.

Minimize the harm by grouping difficult questions, like mortgage applications, into one inquiry and processing them all within two weeks. Since credit scoring models assume you are looking for a single loan and are not trying to obtain multiple at once, they do not penalize you in that situation.

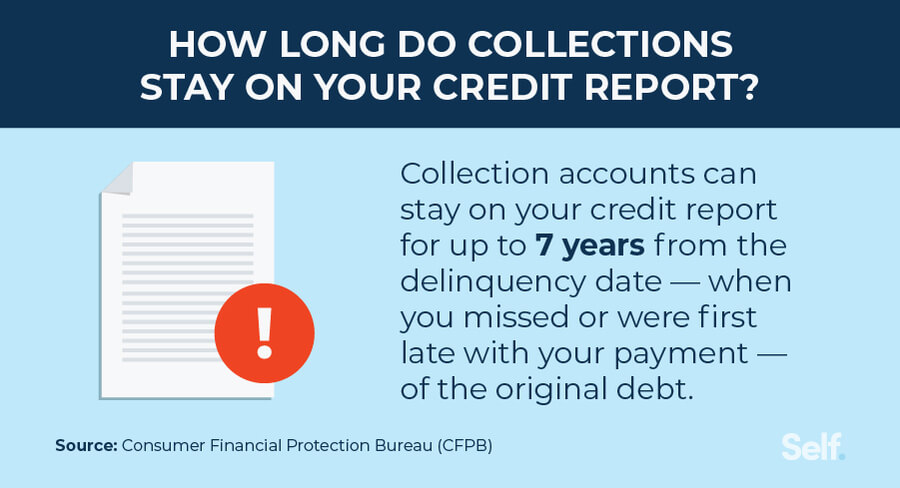

Delinquency: Seven Years

Your credit report may show late payments (typically more than 30 days past due), missed payments, and accounts that have been turned over to a collection agency for seven years following the date of the delinquency.

Minimize the harm by making sure you pay on time or catch up. Call the creditor and request that this infrequent error not be reported to the credit bureaus if you typically pay on time but for some reason missed a payment.

Charge-Off: Seven Years

A charge-off occurs when a creditor writes off your debt as a result of your failure to make payments. Charge-offs can stay on your credit record for a maximum of seven years following the date of the initial payment failure.

Reduce the harm by attempting to settle the debt in full or in part through negotiation. You probably won’t be sued, but the negative mark on your credit won’t go away.

Student Loan Default: Seven Years

Your credit report will contain information about any defaulted student loans for seven years following the date of the default. Federal student loans do not default for nine months, but private student loans can after three months of nonpayment.

Minimize the harm: The Department of Education offers several programs, including loan rehabilitation, loan consolidation, and various repayment plans, that are worthwhile to investigate if you have federal student loans and are having difficulties making repayments. Rehabilitating the loan allows you to have the default removed from your credit report, but the late payment history will still be there. With private loans, contact the lender and request modification.

Foreclosure: Seven Years

When you don’t make your loan payments on time, your lender will take possession of your house through foreclosure. Your credit report will retain this information for seven years following the date of the initial late payment.

Minimize the harm by paying your other debts on schedule and taking action to repair your credit.

Bankruptcy: Seven to 10 Years

Depending on the type of bankruptcy, the period of time it remains on your credit report varies, but it typically lasts between seven and ten years. According to FICO, bankruptcy, sometimes referred to as the “credit score killer,” can lower your credit score by 130 to 150 points. When a Chapter 13 bankruptcy is dismissed or discharged, it usually disappears from your record seven years after the bankruptcy was filed, though in certain circumstances it might stay for ten years. A Chapter 7 bankruptcy will hang around for 10 years.

Limit the damage: Dont wait to start rebuilding your credit. Obtain a secured credit card, make timely payments on any accounts that were not dismissed in your bankruptcy, and only apply for new credit when you are able to manage your debt.

Lawsuit or Judgment: Not Reported

Civil judgments, whether paid or unpaid, used to typically stay on your credit report for seven years after the date of filing. However, all civil judgments were deleted from credit reports by 2018 according to Equifax, Experian, and TransUnion, the three major credit bureaus.

Minimize the harm by ensuring that there are no civil judgments listed in the public records section of your credit reports. If you find one, ask to have it removed.

Tax Lien: Not Reported

Similar to civil judgments, paid tax liens were previously recorded on your credit report for seven years. In nearly all cases, unpaid liens could stay on your credit report indefinitely. Due to false reporting, all tax liens have been removed from credit reports by the three major credit bureaus since 2018.

Minimize the harm by making sure there are no tax liens listed on your credit report. If it appears, report it to the credit bureau in order to have it taken down.

Frequently Asked Questions

At the official website, AnnualCreditReport, you can obtain copies of your credit reports from Equifax, Experian, and TransUnion, the three major credit bureaus. com. You have a legal right to a free report from each bureau once a year or more.

Equifax, Experian, and TransUnion, the three major credit bureaus, are offering free weekly online credit reports at AnnualCreditReport.com through the end of 2023. com due to potential financial difficulties from the coronavirus pandemic.

Can You Have Negative Information Removed From Your Credit Report?

Unless the information is false, there is nothing you can do to get negative information removed from your credit report before it would ordinarily disappear. You can dispute inaccurate information with the credit bureau, which will need to look into it and get back to you. On their websites, the three main bureaus provide an explanation of the process, and you can typically submit your request online.

What Is the Statute of Limitation on Debts?

There are statutes of limitations on debts in most states, usually lasting three to five years, after which time debt collectors cannot pursue legal action against you. They may still make other attempts to collect those debts, though, and they will stay on your credit reports until they cease to exist because of old age.

The Bottom Line

There isn’t much you can do to expedite the removal of negative information from your credit reports unless it is inaccurate, even though most of it will eventually disappear. Therefore, it’s important to continue making your bill payments on time in order to avoid having any bad information appear on your credit report in the first place. Article Sources: Investopedia mandates that authors cite original sources to bolster their claims. These consist of government data, original reporting, white papers, and conversations with professionals in the field. When appropriate, we also cite original research from other respectable publishers. You can read more about the guidelines we adhere to when creating impartial, truthful content in our

When you visit the site, Dotdash Meredith and its partners may store or retrieve information on your browser, mostly in the form of cookies. Cookies collect information about your preferences and your devices and are used to make the site work as you expect it to, to understand how you interact with the site, and to show advertisements that are targeted to your interests. You can find out more about our use, change your default settings, and withdraw your consent at any time with effect for the future by visiting Cookies Settings, which can also be found in the footer of the site.

FAQ

Is it true that after 7 years your credit is clear?

Negative information generally remains on credit reports for about seven years, including late or missed payments, accounts that have been reported to collection agencies, accounts that are not paid as agreed upon, and bankruptcies.

What happens after 7 years of not paying debt?

The good news is that the unpaid debt won’t last forever, even though it will appear on your credit report and lower your score. Unpaid credit card debt disappears from your credit report after seven years. Although the debt doesn’t totally disappear, it will no longer have an effect on your credit score.

What stays on credit report the longest?

Most negative information can typically be reported by a credit reporting agency for seven years. You have seven years to report information about a lawsuit or judgment against you, or until the statute of limitations expires, whichever comes first. Bankruptcies have a ten-year maximum retention period on your record.

Do collections fall off after 7 years?

How long will collections appear on your credit report? Collections, like other negative information, will show up there for seven years. Additionally, a paid collection account will stay on your credit report for seven years.

Read More :

https://www.equifax.com/personal/education/credit/report/articles/-/learn/how-long-does-information-stay-on-credit-report/

https://www.consumerfinance.gov/ask-cfpb/how-long-does-negative-information-remain-on-my-credit-report-en-323/