Types of Credit Cards

Various credit card kinds meet the needs of various spender types. To keep things simple, choose the one that best suits the user’s financial goals. For example, someone who doesn’t spend a lot of money and is only concerned with getting the most value for their money can probably get by with a no-fee cash back card. Even though it takes some management, it is very feasible for people to carry multiple credit cards due to their various benefits. The most crucial thing is that they are all settled on time.

Cashback: These offer cashback on all purchases, usually 1%, 1. 5%, or 2%. Another kind of payment option could offer up to 5% back on specific product or service categories, which are typically rotated every quarter.

Rewards: These make up the bulk of most credit cards. Typically, the rewards come in the form of hotel reservations, dining benefits, and airline miles. More miles or rewards on credit cards typically come with annual fees. It is up to the individual spender to assess their spending patterns and determine whether a no-fee or low-fee card with low rewards is better than a high-fee card with high rewards.

Charge: These typically function in the same manner as any other credit card, with the exception that they are not eligible for balance rollovers from one month to the next and have either very high or no spending limits. At the end of each month, the holder is supposed to pay the remaining amount in full. The only real advantage of owning one is the ability to spend a lot of money; just be sure to pay it off in full each month.

Balance Transfer: Due to the high interest rates on credit cards, these are ideal for consumers who intend to incur large amounts of debt in the future. An existing balance can be moved from one credit card to another. In contrast to most credit cards, some have introductory APRs that are low or even zero for the first six to twenty-one months, allowing the holder to transfer debt from one card to another effectively interest-free. Credit cards with balance transfers are usually more helpful for those with large existing debt on high APR cards.

Secured: People with poor credit histories or younger individuals interested in starting out can benefit from secured credit cards. An application for a secured credit card requires the payment of a security deposit, which serves as collateral. If the applicant shows that they can manage their finances with the secured credit card and decide they no longer want to use it (many other credit cards are available that do not require a security deposit after meeting the minimum credit score), they can close the account and get their deposit returned.

Prepaid: A prepaid credit card works more like a debit card because it has a limit on the amount that can be loaded onto it. Reloadable, multi-use, and single-use cards are the common types. These are frequently sent back by companies as gifts or as payment for rebates on the products they have purchased.

Store: Some retail establishments provide credit cards with exclusive deep discounts to that specific chain. Typically, a cashier will offer them at department stores during checkout and package them with a discount similar to 2010% on the total amount of purchases. Customers who shop at the stores regularly enough to justify their financial benefits tend to find these to be more beneficial. Additionally, because they frequently accept lower credit scores than other credit cards, they are good choices for those with bad credit who want to rebuild their credit. But compared to other credit card kinds, store credit cards typically have higher interest rates.

Business: Certain cards are designed to support the requirements of businesses. They provide discounts on business-related goods and services, sophisticated cost tracking tools, emergency travel assistance, medical support, and travel agency services, among other things. When it comes tax time, business credit cards help to keep personal and business expenses apart.

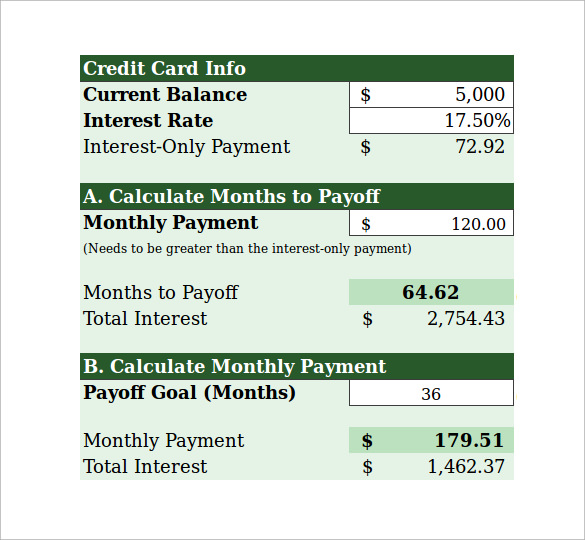

How to Calculate Interest Charges on Credit Cards

Average Daily Balance Method

Generally speaking, credit card companies use the average daily balance (ADB) method to determine the monthly interest payment. Credit card companies use a daily periodic rate, or DPR, to determine the interest charges because the length of the month varies. The DPR is computed by dividing the annual percentage rate (APR) by 365, the number of days in a year.

| Daily Periodic Rate, DPR = |

|

Then find the ADB. To calculate this, use a more laborious equation: add up all of the balances for every day of the statement billing cycle, then divide the total by the number of days in the billing cycle.

| ADB = |

|

Lastly, to calculate the interest for that month’s statement, multiply this by the Daily Periodic Rate that was computed earlier and the total number of days in the billing cycle.

Interest payment each month is equal to DPR × ADB × the number of billing cycle days.

For instance, Jon needs assistance figuring out how much interest he will have to pay on one of his credit cards in June. It carries an APR of 15%. Calculate his DPR using the equation above:

| DPR = |

|

= 0.00041 |

There was $500 outstanding at the end of the June billing cycle’s first 15 days. Jon paid $100 halfway through the month, leaving a $400 balance for the final 15 days. Calculate his ADB utilizing the equation above:

| ADB = |

|

= $450 |

To get the monthly interest payment, multiply the DPR, ADB, and number of days in the billing cycle:

Monthly interest payment = 0. 00041 × 450 × 30 = $5. 54.

Jons interest payment for the month of June is $5.54.

Although they aren’t used very frequently, credit card issuers can also determine the monthly interest payment using the previous balance method and the adjusted balance method.

Previous Balance Method

Divide the DPR by the balance from the previous month and the total number of days in the billing cycle. Assuming that Jon had $300 in his account at the end of the previous month:

Monthly interest payment = 0. 00041 × 300 × 30 = $3. 69.

Adjusted Balance Method

Divide the DPR by the adjusted balance, which is the outstanding balance from the prior month less any payments made. Next, multiply the outcome by the billing cycle’s number of days. Assuming that Jon had a $300 balance at the end of May and had paid $200 so far:

Monthly interest payment = 0. 00041 × (300 – 200) × 30 = $1. 23.

Providers will impose a minimum payment, which is primarily an interest payment, based on the computation of monthly payments. It is important to make this payment. Failing to do so could result in the card being cancelled, legal action being taken, and a sharp decline in the holder’s credit rating.

Interest on the balance of a credit card is relatively high unless it has a zero or low introductory APR. The average credit card annual percentage rate is approximately 2020%, which is a relatively high rate for any type of loan. Excellent APRs typically range from 12% to 20%8, but people with exceptional credit may be able to get even lower rates. This is due to the fact that credit card debt is unsecured, meaning the loan is not secured by any collateral. The lender cannot seize any assets in the event of a borrower default; this risk is reflected in the high interest rate. Secured debt, in comparison, requires collateral, such as real estate. The lender may foreclose and seize the real estate if the borrower defaults on the secured debt.

| Search |

FAQ

How to calculate credit card payment formula?

Determine the interest rate you pay on your card (E2%80%9412%%APR, for instance). Convert that annual rate to a monthly rate by dividing it by 2012%E2%80%94 since a year consists of 2012 months. Therefore, in this example, you would pay 1% per month. Multiply the monthly rate by your outstanding balance. As an example, use 1% times a balance of $7,000.

What is the minimum payment on a $5000 credit card balance?

|

Issuer

|

Standard Minimum Payment

|

|

Capital One

|

$50

|

|

Chase

|

$50

|

|

Citibank

|

$75

|

|

Credit One

|

$250

|

What’s the minimum payment on a $500 credit card?

Method of percentages: A portion of credit card issuers determine the minimum payment by dividing it by the total amount owed. Usually, this percentage lies between 1% and 3%, although it is subject to change. In the event that, for instance, your outstanding balance is $500 and the minimum payment percentage is 2%, your minimum payment would be $10.

How do you calculate a monthly payment?

Therefore, you must divide your interest rate by 12 to get your monthly loan payment. Whatever figure you get, multiply it by your principal. A more straightforward approach is principal x (interest rate / 12) = monthly payment.

Read More :

https://www.bankrate.com/finance/credit-cards/minimum-payment-calculator/

https://www.thebalancemoney.com/calculate-credit-card-payments-and-costs-315644